The most common way to lower your interest rate is done by paying cash up front to the lender for a lower rate – sometimes called discount points. So you buy down your rate. And now that the market is sowing down a bit, seller’s are likely going to be more likely to consider concessions – like a cash contribution to your closing costs which you can use to buy down your interest rate.

So here’s how points work, how much they cost and how much they lower your rate.

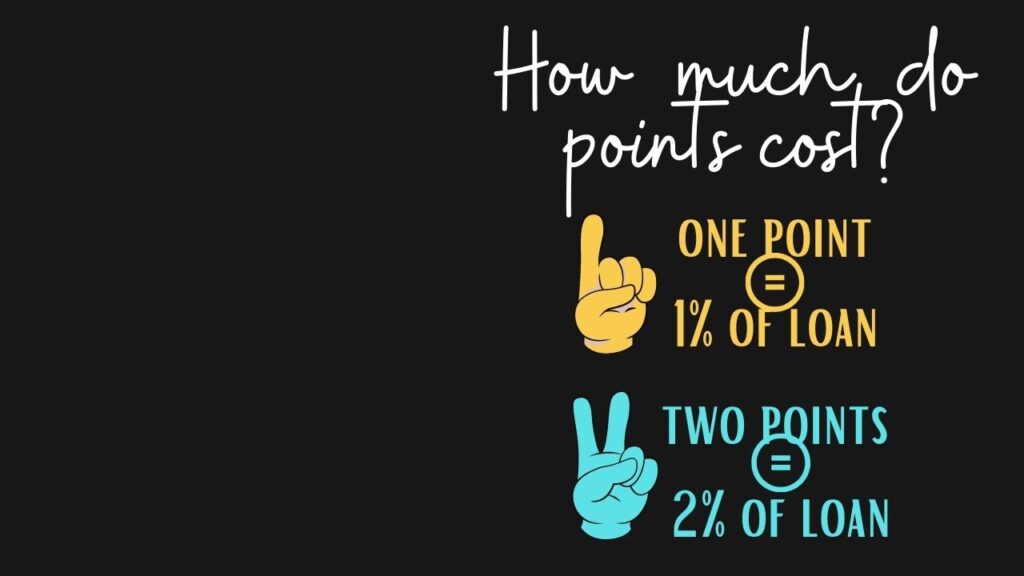

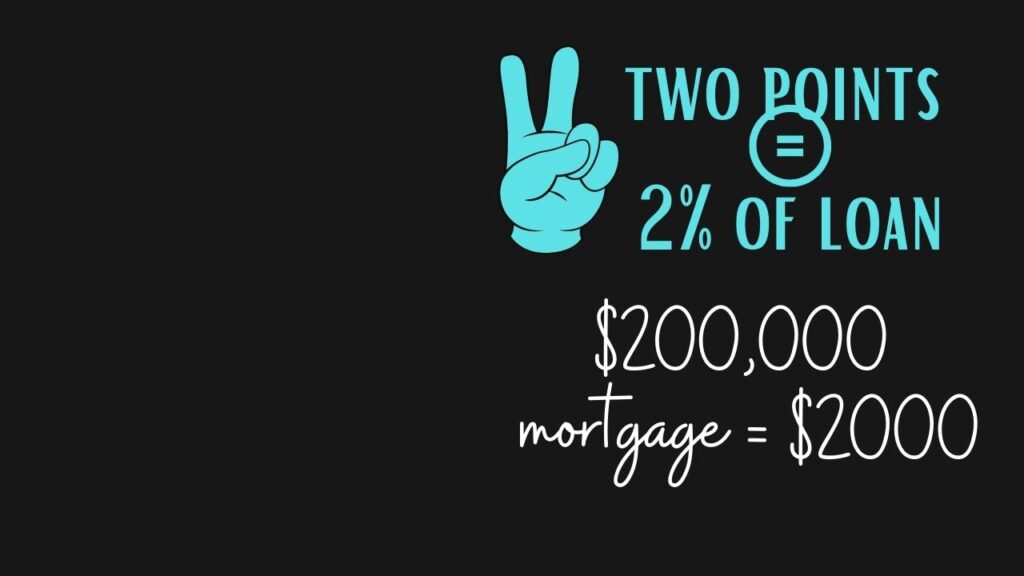

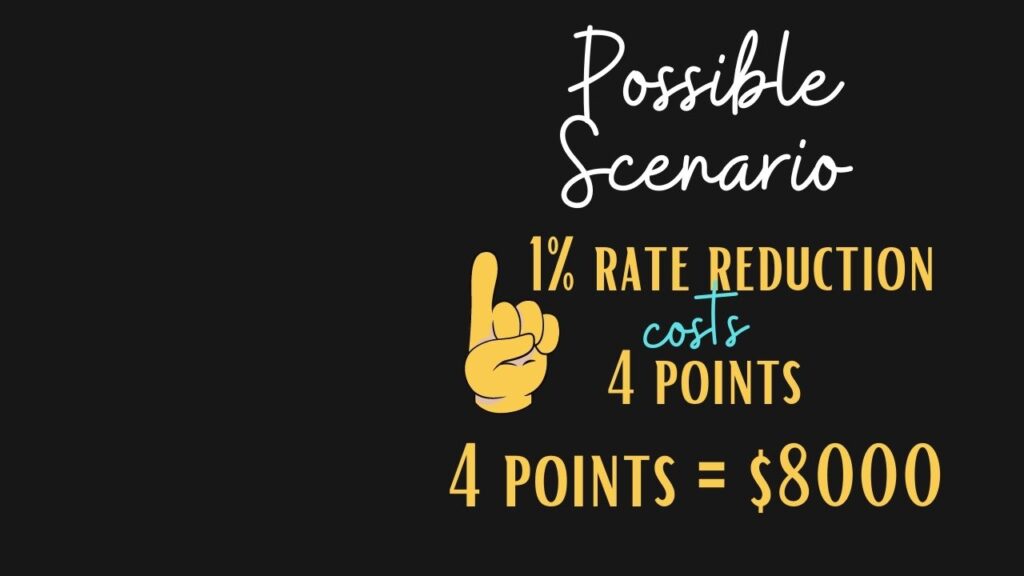

One point will cost 1% of the mortgage amount. For a $200,000 mortgage, one point would equal $2,000, two points – $4,000. A 2 point buydown does not mean your rate will go down 2%. It’s usually a fraction of that – a lender wll likely say something like “decreasing your interest rate by one percent will cost you X discount points. For example, say reducing the rate by 1% will cost four points – $8000 on a $200,000 mortgage. That’s going to vary by lender. But before doing a buydown like this consider how long it will take to pay off that $8000 with the savings it produced. If the rate went from 7% to 6%, your payment will go from $1331 to $1199 a month. that will save you $132 a month. It will take around 5 years at 132 a month to pay off that $8000.

You’ll basically break even in 5 years – so if you are going to be in the house longer than 5 years, it’s very well may be worth it because for the next 25 years after that you’ll have that lower payment.

The rise in interest rates is sort of a good news/bad news kind of thing for buyers.. As the interest rate goes up, the amount of house you can afford goes down. So if at 4% you could afford a $300,000 house – an increase in the rate to 7% is going to increase your payment so now you may have to lower that to the $250,000 range. That’s the bad news. The little bit of good news is higher rates will bring down demand so there’s not as much competition for homes. And that means sellers may be more likely to consider concessions.

And one of those concessions could be a credit or subsidy in the form of a cash contribution to the buyer which could be used to buy discount points to lower the interest rate.

That example is for a permanent buydown where the lower rate lasts for the entire length of the mortgage. Another type of buydown is a temporarty buydown. So you buy down the rate for a limited amount of time. It allows you to lower your interest rate at the beginning of the mortgage but, eventually,your rates will return to “normal.” The most common temporary buydowns are 3-2-1 buydowns – that buys down the rate for 3 years, or 2-1 buydowns – that buys it down for 2 years.

Typically on these temporary buydowns the rate goes up 1% a year till it reaches the permanent rate. . So on a 321 buydown of a 7% rate Year one would be 4%, year 2- 5%, year 3- 6% and then go back to the 7% in year 4 and stay there for the life of the loan.

A temporary buydown will probably cost less upfront but you only get that lower rate for a few years so it’s going to cost more in the long run. You are basically paying for a pre-set adjustable rate. Before going that route, I would check with some local lenders on the terms of a regular adjustable rate and compare the two. You don’t buy points to get an adjustable rate mortgage. There’s a local bank here that offers an adjustable rate mortgage with very low closing costs and no prepayment penalty. If you’d like that contact information, let me know and I’ll send to you.

The main reason to consider the temporary buydown options or an adjustable rate mortgage is if you believe interest rates will go down in the not too distant future and you plan on refinancing when they do. I haven’t seen anything saying interest rates will go down anytime soon. The other reason to consider these options is if you plan on paying off the mortgage fairly soon and want a lower rate until you can do that. If neither of those conditions apply to you, then probably the better option is the permanent buydown depending on how much the lender is going to charge you to get that lower rate and how long it will take to pay off the cost of the buydown with the saving it produced.

So Should you lower your interest rate by buying discount points either a permanent buydown or a temporary buydown or look at a regular adjustable rate mortgage. If you go the permanent route, check how much it costs and how long it will take to pay off the cost of the buydown. If you plan on paying off the mortgage or refinancing in a few years, consider the adjustable rate mortgage or a temporary buydown. If you go for the buydown, you can ask the seller to contribute toward that. If you do decide to ask for a seller concession to buy points or pay closing costs, keep in mind you are lowering your net offer for the house.

So if you offer $300,000 for a house and ask the seller to pay $9000 toward your closing expenses (which you could use to purchase points) your net offer is $291,000. Before the market took off, asking for seller concessions was pretty common. Not so much in the last couple years. But that could change now that the market is slowing down.